Pricing your jewelry can be one of the trickiest aspects of running a jewelry business. We've created an interactive tool and accompanying free webinar to help you make sure you are not only covering your costs but making a living wage.

Jewelers often feel uncertain about pricing their work. It is a common frustration among new artists and experienced professionals alike. This post is packed full of resources to help you understand how to price jewelry. Pricing involves so much more than just the cost of your jewelry making supplies.

Plan Your Jewelry Business

When you are starting a jewelry business, it is more than a full-time job. Even though you may be self-employed, you still should plan for a living wage for your labor including both jewelry production time and administrative time. Industry magazines and books cover this topic with great frequency because it is such a common problem in the world of jewelry and American craft. Many designers do not calculate a sufficient salary into their pricing scheme and end up barely covering their costs. Other overhead costs are often ignored altogether.

There is no one hourly wage or annual salary that fits every operation. As an entrepreneur, it is easiest to start with the standard of living you are accustomed to and work backward through the numbers to determine your price per item. Consider salary along with your pricing in order to match your revenue needs with a cost analysis.

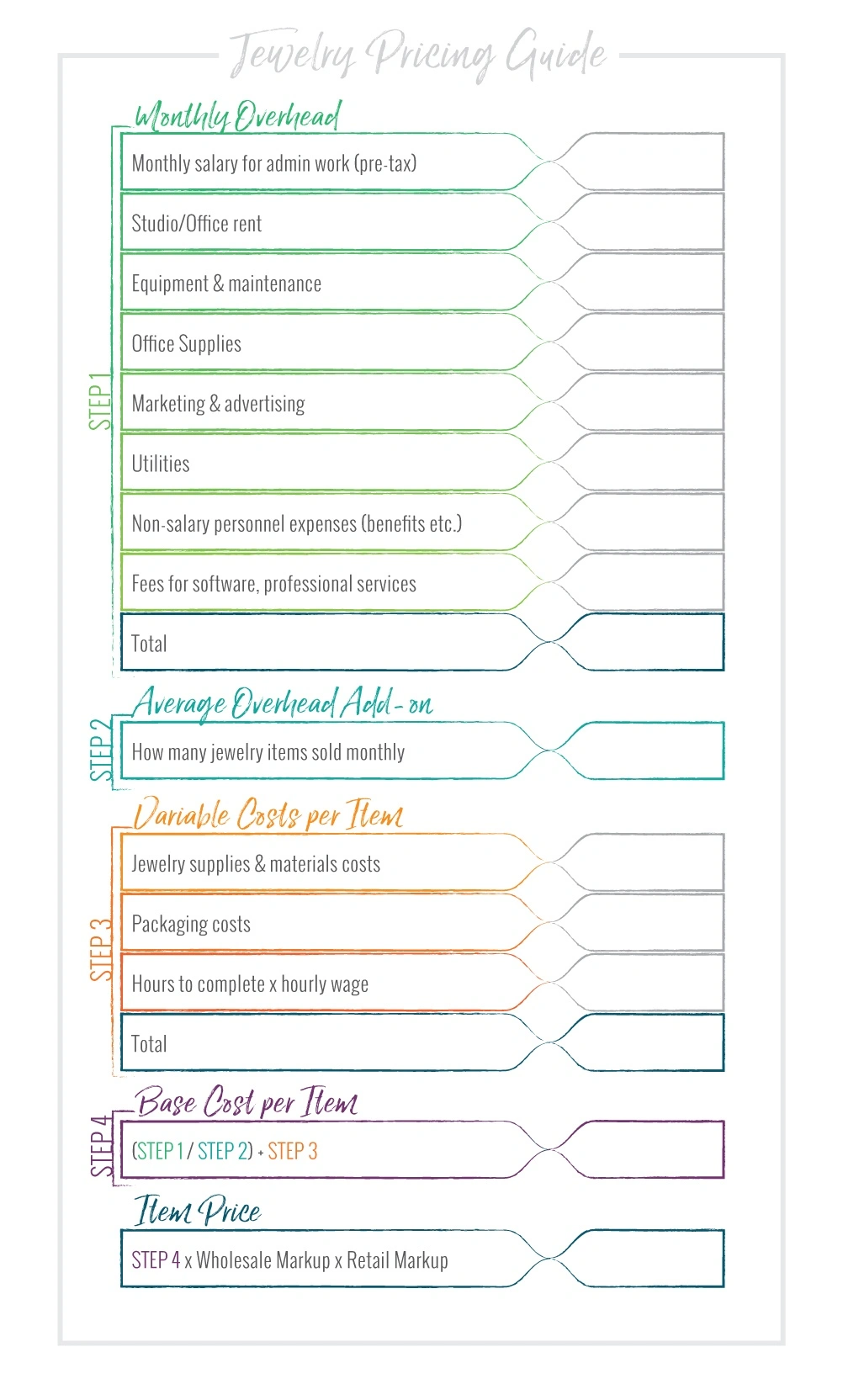

Jewelry Pricing Worksheet Tools

We developed the following simplified worksheet to help you analyze your finances and price your jewelry accordingly. This graphic is a quick template to make sure you consider all the different cost inputs before setting a price. It includes your monthly jewelry volume in order to help you allocate your overhead costs across all the jewelry pieces you sell. The result is a base price to consider for your jewelry piece. Keep in mind, formulas like this are meant to be tools to stimulate thinking. The result provides feedback to you as the maker, but it is not the "right" price. It is a guideline calculation. You will need to add your wholesale and retail mark-ups. Then, also consider your competition, your brand, and your target audience before settling on a price amount.

For a more in-depth experience, click this link to download a copy of our interactive jewelry pricing guide. It is a file in Google Docs that allows you to experiment with different variables in your jewelry work and your jewelry business to better understand how your pricing and your salary are interrelated. Tinker with the tool to try out different jewelry pieces, different cost inputs, and different production volumes. Think about where your business is now and where you would like it to be once you meet your goals. Be sure to read all the instructions and visit the final FAQ page to get the maximum value out of this resource. DOWNLOAD THE INTERACTIVE WORKSHEET >>

Overhead and Variable Costs

Fundamentally, your costs are divided into overhead and variable costs. Overhead costs are fixed and do not vary based on the number of items you produce. Nonetheless, they are still business expenses that must be covered by your sales. Variable costs are the labor and materials that go into each piece of jewelry. These costs depend on your production volume and the specific designs being made. Both figures should be calculated into your pricing scheme.

You will probably have to make some assumptions if you don't know all of the numbers required, or if you are projecting rapid growth. Play with various figures to get an idea of how they affect the pricing formula. We recommend counting your administrative salary separately from your hourly production wage, even if you perform both duties. If you are creating a jewelry line you will eventually need to hire employees. This labor will be a separate expense. It is better to plan for that ahead of time and make sure your pricing covers staffing. Likewise, if you are currently working out of a home office but will need to expand into a studio space soon. Think ahead when planning your costs.

For the chart above, divide the Step 1 total by the number of jewelry items you sell monthly. Add the Step 2 total and the Step 3 total to get the base cost for a piece of your jewelry that includes all your cost inputs. This worksheet yields your minimum price to break even and cover your expenses. It leaves you with no working capital to invest in the creation of new product lines or business development activities. It does not cover losses from dead inventory that never sells or sits on the shelf for many months before converting into revenue. Furthermore, it does not yield a net profit after paying your bills.

Retail and Wholesale Jewelry Markup

There are many pricing formulas referenced in the jewelry field. Some formulas markup your (materials cost + labor cost) by 2 for wholesale and then again by 2 times for retail. The markups you use will depend on the materials you work in and competition for your style of work. There is no one method that is best for all jewelry. For example, base metal jewelry often has a larger markup multiplier than gold and platinum.

Whichever formula you choose, it is important to mark-up your base price for both wholesale and retail sales. Be sure to leave a significant gap between the two. If you take on wholesale accounts, they will need reassurances that there is room for them to sell the line profitably and that you will not compete against them and undercut their pricing. Even if you only plan to sell directly to consumers at retail, leave a wholesale margin in place in case you pivot strategically down the road.

About The Halstead Grant and Halstead Jewelry Supplies

The Halstead Grant application is another powerful tool for examining your business. In it are several questions about pricing strategy, how you will pay yourself, and build your business. The Halstead Grant application process can be used as a template to help you set goals for your business and create a pricing plan that works for you. Download an application and think about the questions as an exercise to develop your small business strategy. It is worthwhile even if you are not eligible to apply.

Halstead is one of North America's leading distributors of quality jewelry supplies. Halstead specializes in wholesale findings, chain, and metals for jewelry artists.

How Perceived Value Affects Jewelry Pricing

Wise marketers know that their customers care about more than just the price tag when they are buying jewelry. Shoppers are constantly assessing value, which is a more complicated judgment based on the perceived worth of what they get in exchange for their money. Adding a few premium options to pieces in your line can widen your selection of price points during the key holiday season. Here are some ideas.

1. Add a 14kt solid gold charm

Small solid gold charms start at just a few dollars, but they give you more latitude in pricing a finished piece. Consider adding one 14kt solid gold charms to a cluster of sterling charms or a bracelet. The mixed metal look is popular and adding a small 14kt gold accent allows a customer to feel like the piece is of higher value.

2. Add a gemstone charm

Similarly, consider adding a diamond or gemstone to your piece. You will be surprised at how affordable many precious stones can be. We carry a small selection of silver gemstone charms that start at just a couple dollars each. A touch of sparkle is always a big hit with customers!

3. Customize

Customers place high value on customizations such as personalized stamped charms or engravings. Make sure you upsell this option as long as you have time available in the studio.

4. Packaging

Trite as it may seem, luxurious packaging makes your beautiful jewelry look even better. Don't settle for just run of the mill jewelry boxes. Add fine ribbons, feathers, floral elements and custom labels to make your packaging really pop. Shoppers swoon over beautiful bags, boxes and bows. Keep your packaging on brand for your business. If you're selling at a high price point, luxurious packaging is a must. If your pieces are a little more natural feeling, use packaging that gives off the same vibe. Learn more about creating your jewelry brand.

5. Presentation

Fine jewelry stores know that the way you handle your jewelry when you show it to customers is critical. This is why fine jewelers usually place items on a velvet pad or silver tray when they take them out of the case for customers to try on. They could just hand the jewelry straight to the customer, but the presentation is part of the sales technique. Think about your displays and how you handle your products in front of clients. What does it say about the value of the work and the materials. How can you convey value with your non-verbal actions? Be sure to translate this presentation to your online presence with professional jewelry photos.

Halstead Jewelry Supplies sponsors education and community content like this to help all jewelry artists in the field. Please consider sourcing your chain, findings, and materials from Halstead. We've been serving the trade from Northern Arizona for over 50 years!